Categories

Buyers and Sellers, Real Estate, Real Estate TipsPublished February 6, 2026

The "Highest Offer" Trap: Why the Best Bid Isn't Always the Biggest Number

By Adam Martin Team Lead, Loxley Martin | Top-Rated Dayton & Greene County Realtor

It is the moment every seller dreams of. We list your home on Thursday. By Sunday night, we are sitting at your kitchen table with five different offers spread out in front of us.

- Offer A: $300,000

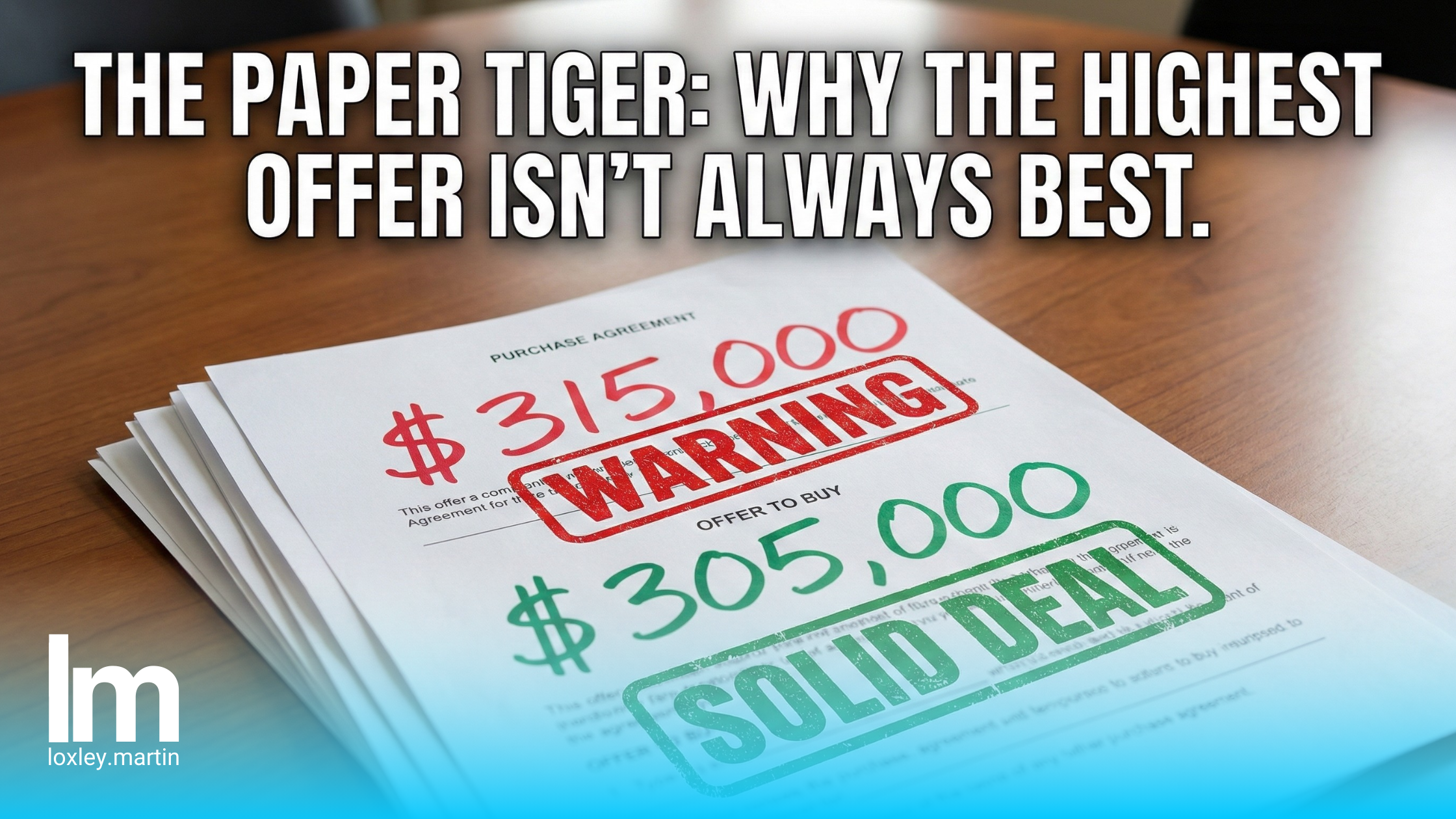

- Offer B: $305,000

- Offer C: $315,000

Your eyes immediately go to Offer C. It’s $15,000 over list price! It looks like the clear winner. But as your agent, I have to be the one to tell you: "Be careful. Offer C might actually be the worst one here."

In a hot market like Dayton’s, getting multiple offers is common. But evaluating them is where the "pros" earn their commission. The highest price is often a "Paper Tiger"—it looks scary and big, but it falls apart the moment you poke it.

Here is how we evaluate multiple offers to ensure you actually make it to the closing table.

1. The "Financing" Stress Test

The first thing I look at isn't the price; it’s the financing method. A $315,000 offer is worthless if the bank won't lend the money.

- Cash is King: If a buyer has cash, there is no appraisal and no lender underwriting. It is the surest bet.

- Conventional Loans: These are strong, usually requiring 5-20% down.

- FHA/VA Loans: I love my military VA buyers (especially near Wright-Patt!), but as a seller, you need to know these loans have stricter appraisal and inspection requirements.

The Trap: Offer C ($315k) might be an FHA loan with 3.5% down. If the appraisal comes in low, they have no cash to bridge the gap. Offer B ($305k) might be Conventional with 20% down. Offer B is often the safer bet.

2. The Appraisal Gap Guarantee

This is the single most important clause in a 2025 contract. If Offer C offers $315,000 but the house is only worth $300,000, what happens?

- Without a Gap Clause: The deal stalls. The buyer asks you to drop the price to $300,000. You are right back where you started.

- With a Gap Clause: The buyer promises to pay the difference in cash.

Adam’s Rule: I never look at the "Offer Price." I look at the "Appraisable Price." If they offer $315k but don't waive the appraisal, they are really only offering $300k.

3. The "Escalation Clause" (The Secret Weapon)

You might see an offer that says: "I will pay $300,000, but I will beat any other offer by $1,000 up to a cap of $320,000." This is called an Escalation Clause.

- Why it’s great: It shows the buyer is serious and willing to fight.

- The Catch: We need to see the "Cap." If their cap is $320,000, that’s great. But we also need to make sure they have the cash to cover that higher price if the appraisal doesn't keep up.

4. The Contingency Check (The Exit Ramps)

Every contingency is an "Exit Ramp" for the buyer to walk away with their earnest money.

- Inspection Contingency: Did they ask for a "Pass/Fail" inspection (good) or a full negotiation period (risky)?.

- Home Sale Contingency: Do they have to sell their house in Huber Heights before they can buy yours? In a multiple-offer situation, I almost always advise avoiding these unless the buyer is already under contract.

5. The "Lender" Reputation

This is a small detail that matters. Who wrote the pre-approval letter?

- Is it a trusted local lender in Beavercreek who picks up the phone on weekends?.

- Or is it a 1-800 number from an internet bank?

Local lenders have a reputation to protect. If a local loan officer tells me the buyer is solid, I believe them. If an internet algorithm says it, I’m skeptical.

The Bottom Line

Don't get blinded by the big number. A $305,000 offer that closes in 30 days with no hassle is worth infinitely more than a $315,000 offer that falls apart a week before moving day.

We pick the offer that closes. Not just the one that sparkles.

Have a Stack of Offers?

Or expecting one? Don't navigate the fine print alone. I use a "Multiple Offer Spreadsheet" that breaks down every bid side-by-side: Net Price, Gap Coverage, Inspection Terms, and Lender Quality.

Adam Martin Team Lead, Loxley Martin Your Dayton & Greene County Real Estate Expert

Adam Martin

| LoxleyMartin | Howard Hanna

or another way