Categories

Local News, Real Estate, Real Estate TipsPublished January 9, 2026

The "Appraisal Trap": What Happens When the Bank Disagrees with the Price?

By Adam Martin

Team Lead, Loxley Martin | Top-Rated Dayton & Greene County Realtor

It is the phone call no seller wants to receive two weeks before closing.

We are under contract. The inspection is done. The buyer is excited. And then the lender’s appraisal comes back.

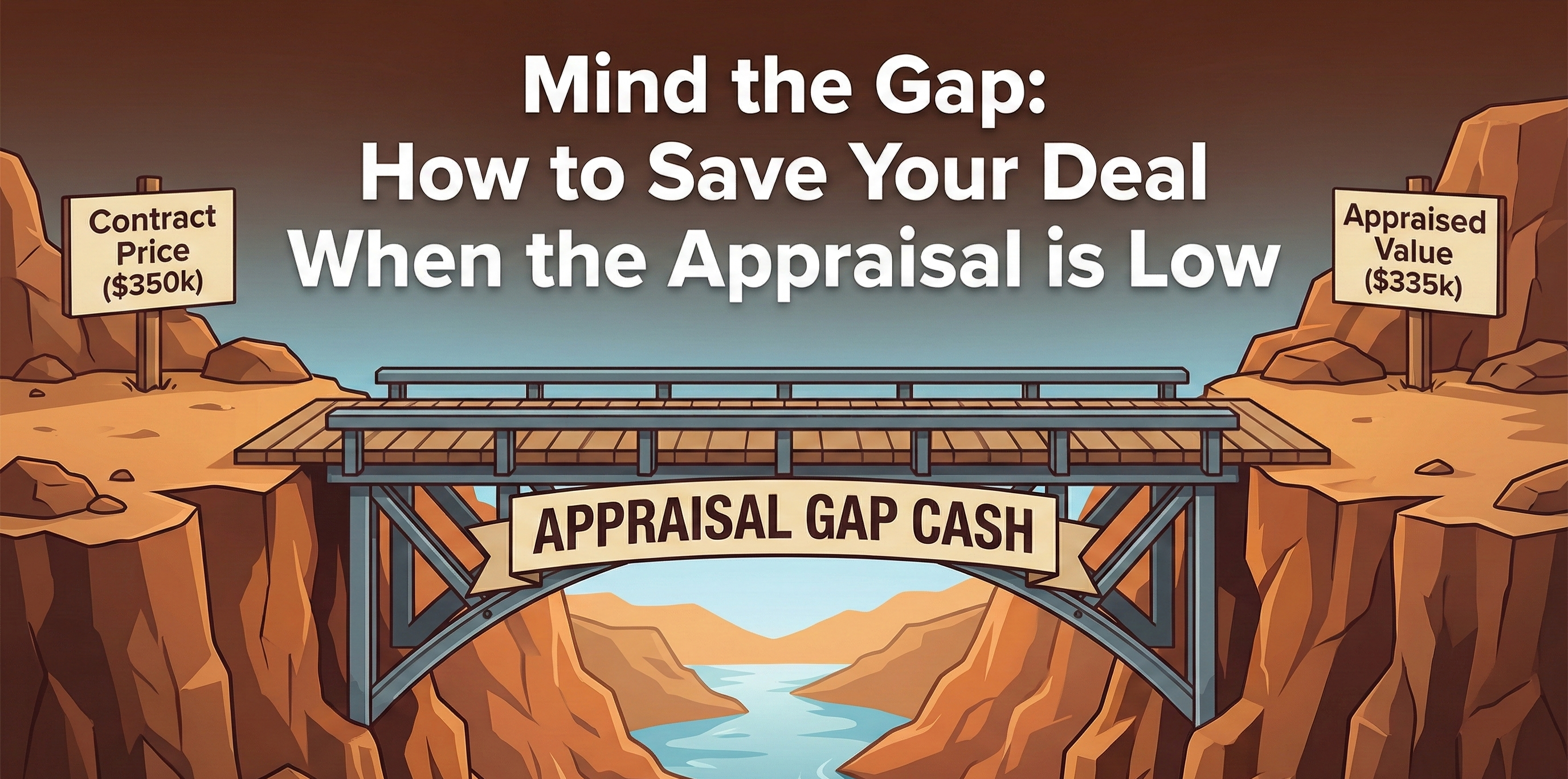

- Contract Price: $350,000

- Appraised Value: $335,000

Suddenly, we have a $15,000 hole in the deal. The bank is saying, "We don't care what the buyer wants to pay; we are only lending on $335,000."

In a market like Dayton’s, where prices have risen nearly 8% in some areas over the last year, this is becoming a common headache. Appraisers are looking at "sold" data from 6 months ago, but we are selling in today's market. The data often lags behind reality.

So, what happens next? Does the deal die? Do you lose $15,000? Not if you have the right strategy.

Option 1: The "Appraisal Gap" Clause (The Proactive Move)

Ideally, we win this battle before we even accept an offer.

When I review offers for my sellers, I am looking for an Appraisal Gap Guarantee. This is a clause where the buyer promises to cover the difference in cash if the appraisal comes in low.

- Example: A buyer offers $350k with a "$10,000 Gap Coverage."

- If the house appraises at $340k, the buyer is contractually obligated to bring that extra $10k cash to closing.

- Without this clause, you are negotiating from zero. With it, you are protected.

Option 2: The Negotiation (The Compromise)

If we don't have a gap clause, we have to go back to the bargaining table. We essentially have three choices:

- Seller Drops Price: You lower the price to $335,000 to match the appraisal. (I rarely advise this as a first step).

- Buyer Pays Cash: The buyer makes up the entire $15,000 difference out of pocket. (Great if they have it, but many first-time buyers don't).

- Meet in the Middle: This is the most common Dayton solution. You drop to $342,500, and the buyer brings $7,500 extra cash. Everyone feels a little pain, but the deal closes.

Option 3: The Dispute (The Hail Mary)

Can we fight the appraiser? Yes, but it is an uphill battle. This is called a Reconsideration of Value (ROV).

I have successfully fought these, but only when I can prove the appraiser made a factual error.

- Did they miss the fact that you have a finished basement?

- Did they use a "comp" from a different school district that sells for 20% less?

- Did they ignore a recent sale in your neighborhood that supports our price?

If the appraiser was lazy, we challenge it. If they just disagree with the market heat, we usually move to Option 2.

The "Wright-Patt" Factor: VA Appraisals

A special note for my Greene County sellers: If your buyer is military using a VA Loan, the appraisal stays with the house for six months.

If a VA appraiser values your home low and the deal falls through, that low value is "stuck" to your property for the next VA buyer. This is why vetting the buyer's lender matters. We need local lenders who know that a house in Beavercreek is not the same as a house in Riverside, even if they are miles apart.

The Bottom Line

A low appraisal doesn't mean the deal is dead. It just means the negotiation has restarted.

But the best defense is a good offense. This means pricing the home correctly to justify the value to an appraiser and selecting the right offer (not just the highest one) that has the cash strength to survive a low valuation.

Don't let a bank's opinion ruin your sale.

Worried about your home's value?

Let’s make sure we price it to appraise and sell for top dollar.

I offer a Pre-Appraisal Audit as part of my listing consultation. I look for the potential red flags an appraiser will see before they ever step foot in your door.

👉 Want to be safe?

Adam Martin

| LoxleyMartin | Howard Hanna

or another way